Learn how to benefit from Installment Loans for long-term use

A Comprehensive Overview to Home Loans: Solutions and Options Explained

Charting the globe of home mortgage can be intricate. Numerous choices exist, each with distinct attributes and ramifications for prospective homeowners. Recognizing the distinctions between standard and government-backed loans is necessary. Moreover, the application procedure includes careful paperwork and pre-approval actions that many overlook. As borrowers start on their home-buying trip, understanding how to handle these duties efficiently might suggest the distinction in between economic security and difficulty. What techniques can encourage them on this path?

Understanding Home Loans: Types and Terms

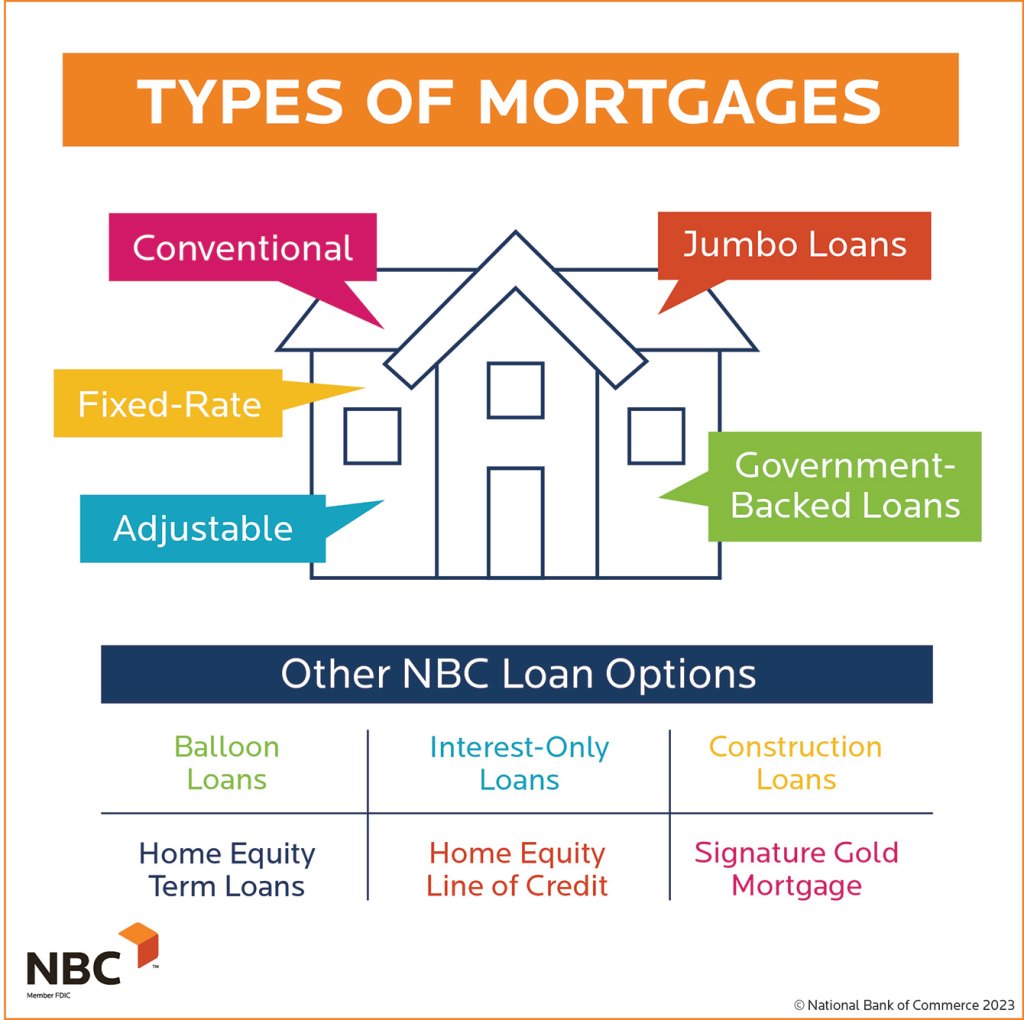

Recognizing the various sorts of home lendings and their linked terminology is essential for prospective homeowners, as it equips them with the knowledge needed to make educated financial choices. Home finances can be broadly categorized into fixed-rate and adjustable-rate home mortgages. Fixed-rate mortgages keep a consistent rate of interest over the life of the loan, providing stability in month-to-month repayments. Alternatively, adjustable-rate mortgages include passion rates that may vary after a preliminary set duration, potentially resulting in lower preliminary repayments however boosted future expenses.

Additional terms is essential for clearness. Principal refers to the car loan amount borrowed, while interest is the expense of borrowing that quantity. The term of the car loan indicates its duration, usually varying from 15 to thirty years. Recognizing these essential ideas allows prospective customers to navigate the complex landscape of home financing, ensuring they select the right loan choice that lines up with their monetary situation and long-term objectives.

Standard Lendings vs. Government-Backed Loans

A significant distinction in home financing exists in between conventional finances and government-backed finances, each accommodating various borrower demands and scenarios. Standard loans are not guaranteed or ensured by the federal government and usually call for higher credit history and down settlements. They are commonly appealing to debtors with secure financial backgrounds, as they might offer competitive rate of interest and terms.

On the other hand, government-backed loans, such as FHA, VA, and USDA fundings, are developed to aid certain teams of customers, consisting of new buyers and veterans. These lendings usually include lower down repayment needs and even more adaptable credit rating requirements, making them obtainable to a broader range of individuals.

Ultimately, the selection between traditional and government-backed car loans rests on the debtor's financial scenario, long-term objectives, and eligibility, making it vital to meticulously evaluate both alternatives prior to making a decision.

The Role of Passion Prices in Home Funding

Rate of interest play an essential duty in home financing, affecting consumers' choices in between set and variable rate finances. The option between these alternatives can substantially influence month-to-month payments, influencing general affordability. Comprehending just how rate of interest work is important for any person steering with the mortgage procedure.

Taken Care Of vs. Variable Prices

Buyers deal with a necessary decision when picking between repaired and variable rates, as this option greatly influences the cost of financing with time. Fixed-rate home loans supply stability, securing in an interest rate for the life of the car loan, which can be beneficial in an increasing rate of interest atmosphere. This predictability enables homeowners to budget plan better. On the other hand, variable-rate home mortgages, or variable-rate mortgages (ARMs), normally begin with lower preliminary rates that can rise and fall based on market problems. While this may result in lower first repayments, consumers encounter the threat of increased rates in the future. Eventually, the choice in between fixed and variable prices depends on individual monetary scenarios, threat resistance, and expectations pertaining to future interest rate fads.

Effect on Monthly Payments

When assessing home financing choices, the influence of rate of interest on monthly payments is a crucial factor to consider. Rate of interest directly affect the general expense of loaning, impacting just how much a consumer will pay monthly. A reduced rates of interest cause smaller sized regular monthly payments, making homeownership much more budget friendly. Conversely, higher prices can considerably raise month-to-month obligations, potentially straining a property owner's budget plan. In addition, the car loan term plays an important role; longer terms might spread repayments out however can result in paying even more passion over time - Fast Cash. Understanding how rates of interest interact with lending quantities and terms is necessary for debtors to make educated economic decisions and pick a home loan that lines up with their lasting monetary objectives

Home Loan Brokers vs. Straight Lenders: Which Is Right for You?

When thinking about a home loan, possible debtors should recognize the unique duties and duties of home mortgage brokers and straight lending institutions. Each option provides its own advantages and drawbacks, which can significantly affect the total cost of funding. An informed option calls for mindful evaluation of these aspects to determine the most effective suitable for individual needs.

Functions and Obligations Defined

Maneuvering the complexities of home funding needs a clear understanding of the functions and duties of home loan brokers and straight lending institutions. Fast Cash. Home mortgage brokers work as middlemans, linking debtors with Homepage loan providers. They analyze try this site a consumer's monetary situation, curate loan alternatives, and guide customers via the application procedure, typically leveraging numerous lending institution connections to secure desirable terms. On the other hand, straight lending institutions, such as banks and credit score unions, give loans directly to borrowers. They manage the whole lending process, from application to funding, with a concentrate on their very own items. Each choice provides unique opportunities for acquiring funding, making it crucial for consumers to review their demands and choices when choosing between engaging a home mortgage broker or functioning with a direct loan provider

Benefits and drawbacks Contrast

Picking between a home mortgage broker and a direct loan provider can significantly affect the home financing experience, as each option offers special benefits and drawbacks. Home loan brokers function as intermediaries, giving accessibility to multiple loan providers and possibly far better rates, while streamlining the finance process. They may charge costs and depend on compensation structures that could affect their suggestions. On the other hand, direct lenders enhance the procedure by using in-house financings, which can cause faster approvals and less problems. Alternatively, they may have a minimal selection of items and much less flexibility relating to pricing. Eventually, the decision pivots on private preferences, monetary scenarios, and the desired level of assistance throughout the home loan trip.

Cost Ramifications Assessed

While assessing the price ramifications of home loan brokers versus direct lenders, prospective homeowners have to consider numerous factors that can greatly impact their general expenditures. Home loan brokers typically bill fees for their solutions, which can vary substantially, influencing the overall financing expense. They usually have access to a wider array of financing items and competitive prices, potentially conserving borrowers money in the long run. On the other hand, straight lending institutions might provide a more simple process with potentially reduced upfront prices, yet their car loan alternatives may be restricted. It is important for homeowners to compare rate of interest, fees, and terms from both brokers and lending institutions, guaranteeing they make an enlightened choice that straightens with their financial objectives and requirements.

The Mortgage Application Refine: What to Expect

The home mortgage application process can commonly feel intimidating for many candidates. It generally starts with collecting required documents, visit this site right here consisting of proof of income, credit rating, and individual recognition. Lenders use this information to examine the candidate's financial security and determine lending qualification.

Next, applicants submit an official application, which might entail filling in on-line kinds or offering information in person. Throughout this phase, lenders examine different variables, such as debt-to-income ratio and credit history, to make a decision on financing terms.

Once pre-approved, the loan provider will certainly perform a comprehensive assessment of the residential property to identify its value aligns with the funding quantity. This phase may likewise include extra history checks.

After last approvals and problems are met, the financing is processed, resulting in the closing stage. Understanding each step encourages candidates, making the trip smoother and much more manageable as they move towards homeownership.

Tips for Handling Your Mortgage Properly

Effectively steering the home mortgage application procedure is just the beginning of an accountable financial trip. Managing a home lending requires interest to a number of key techniques. Consumers ought to develop a clear budget plan that suits regular monthly home mortgage payments, building tax obligations, and insurance. Consistently evaluating this budget plan aids protect against overspending and assurances timely settlements.

Additionally, making additional repayments when feasible can substantially reduce the funding principal and overall passion paid with time. Consumers must also preserve open lines of communication with their loan provider, particularly in times of financial problem - copyright. This can lead to possible services such as car loan modifications or re-financing choices

Finally, it is suggested to keep track of credit rating regularly. A great credit history can give opportunities for far better lending terms in the future. By adhering to these tips, homeowners can browse their funding duties effectively, guaranteeing lasting monetary health and wellness and stability.

Frequently Asked Inquiries

What Are Closing Prices and Just How Are They Determined?

Closing costs encompass fees associated with finalizing a home mortgage, consisting of appraisal, title insurance policy, and financing source fees. These prices commonly vary from 2% to 5% of the loan amount, varying based on area and lending institution.

Can I Get Approved For a Mortgage With Bad Credit Scores?

Yes, individuals with bad credit can receive a mortgage, though choices might be restricted. Lenders commonly need higher deposits or rates of interest, and checking out government-backed financings may boost chances of authorization.

What Is Home mortgage Insurance coverage and When Is It Needed?

When a debtor makes a down payment of much less than 20%, home mortgage insurance policy safeguards lending institutions against default and is normally called for. It assures that lending institutions recoup losses if the borrower stops working to pay back the financing.

Exactly How Does Refinancing Job and When Should I Consider It?

Refinancing involves replacing a present home loan with a brand-new one, generally to secure a lower rate of interest or adjustment financing terms. House owners need to take into consideration re-financing when passion prices go down considerably or their financial scenario boosts.

What Takes place if I Miss a Home Mortgage Payment?

If a mortgage repayment is missed, the loan provider normally assesses late charges, reports the delinquency to debt bureaus, and may initiate repossession process if payments continue to be neglected, at some point endangering the house owner's property.

Fixed-rate home loans preserve a consistent interest price over the life of the loan, providing security in regular monthly repayments. A significant difference in home funding exists between conventional lendings and government-backed loans, each catering to different borrower demands and scenarios. In contrast, government-backed financings, such as FHA, VA, and USDA fundings, are developed to aid particular groups of debtors, including newbie homebuyers and veterans. Rate of interest rates play an essential function in home funding, affecting borrowers' decisions between set and variable rate loans. Fixed-rate mortgages offer security, locking in a passion rate for the life of the finance, which can be useful in an increasing interest rate setting.